The PRMIA 8010 Operational Risk Manager (ORM) Exam validates your ability to identify, assess, and manage operational risks across financial institutions. This certification is designed for risk professionals, compliance officers, and operational managers who need to demonstrate competency in Operational Risk Management frameworks and practices. This landing page provides a structured study roadmap, syllabus overview, and practical preparation guidance to help you pass confidently. Whether you are new to operational risk or advancing your credentials, understanding the exam's scope and question types is essential for effective preparation.

Use this topic map to guide your study for PRMIA 8010 (Operational Risk Manager (ORM) Exam) within the Operational Risk Management path.

The 8010 exam uses multiple-choice and scenario-based items to assess both conceptual knowledge and practical decision-making in operational risk contexts. Questions progress in difficulty, requiring you to apply frameworks to realistic situations.

Questions emphasize practical judgment: you must not only know definitions but also recognize which control, process, or governance approach fits a specific operational risk scenario.

An effective study plan maps each topic to weekly learning goals, balances theory with practice questions, and includes timed review sessions. Dedicate time to understanding how Classic Credit Products, Credit Life Cycle, and Risk Mitigation concepts connect in operational workflows, then layer in advanced topics like CVA and counterparty risk management.

Explore other PRMIA certifications: view all PRMIA exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to 8010 and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test, or get a bundle discount for both formats: Operational Risk Manager (ORM) Exam.

Operational Risk Management frameworks and Risk Mitigation strategies typically account for a significant portion of the exam, as they directly apply to day-to-day operational decisions. However, credit-related topics, especially Credit Life Cycle, Credit Risk Methodology, and Counterparty Risk Management, form the foundation; expect roughly 40-50% of questions to test credit and operational integration. CVA and modern credit modeling are also heavily tested because they represent current industry practice.

A credit product (e.g., a loan or derivative) enters the organization at origination and moves through stages of execution, settlement, and monitoring. At each stage, operational risks emerge, pricing errors, settlement failures, counterparty default. Risk Mitigation controls (collateral management, netting, hedging) are embedded into the life cycle to reduce losses. Understanding this flow helps you answer scenario questions that ask: "Where should a control be placed?" or "What is the operational consequence of this failure?"

Direct experience in credit operations, risk management, or compliance is valuable but not required; the exam tests conceptual frameworks and decision-making, not software-specific skills. If you lack operational background, prioritize understanding the Classic Credit Life Cycle and how operational risks manifest at each stage, then study Risk Mitigation and CVA governance in detail. Real-world case studies and scenario practice questions are your best substitute for hands-on experience.

Candidates often confuse credit risk (the risk a counterparty will default) with operational risk (the risk of loss due to failed processes or controls). Another frequent error is memorizing definitions without understanding how controls fit into workflows; scenario questions require you to apply concepts, not recite them. Finally, many test-takers underestimate CVA and counterparty risk topics, which account for 15-20% of the exam and require both conceptual and quantitative reasoning.

In the final week, shift focus from new content to active recall and scenario practice. Spend 60% of your time on timed practice tests and scenario drills, 30% on reviewing weak-area explanations, and 10% on a final skim of regulatory definitions and key frameworks. Avoid cramming new topics; instead, use practice questions to reinforce connections between Classic Credit Products, Risk Mitigation, and CVA governance. On the day before the exam, do a light review of high-weight topics and get adequate rest.

Which of the following is not a permitted approach under Basel II for calculating operational risk capital

The Basel II framework allows the use of the basic indicator approach, the standardized approach and the advanced measurement approaches for operational risk. There is no approach called the 'internal measurement approach' permitted for operational risk. Choice 'a' is therefore the correct answer.

For a group of assets known to be positively correlated, what is the impact on economic capital calculations if we assume the assets to be independent (or uncorrelated)?

By assuming the assets to be independent, we are reducing the correlation from a positive number to zero. Reducing asset correlations reduces the combined standard deviation of the assets, and therefore reduces economic capital. Therefore Choice 'b' is the correct answer.

Note that this question could also be phrased in terms of the impact on VaR estimates, and the answer would still be the same. Both VaR and economic capital are a multiple of standard deviation, and if standard deviation goes down, both VaR and economic capital estimates will reduce.

The principle underlying the contingent claims approach to measuring credit risk equates the cost of eliminating credit risk for a firm to be equal to:

Under the contingent claims approach, a firm will default on its debt when the value of its assets fall to less than the face value of the debt. Debt holders can protect themselves against such an event by buying a put on the assets of the firm, where the strike price is equal to the value of the debt. In other words, Risky Debt + Put on the firm's assets = Risk free debt. This is because if the value of the assets is greater than the value of the debt, they will be paid in full. If the value of the assets is lower than the value of the debt, they will exercise the put and be paid in full.

Therefore the value of the put on the firm's assets with a strike equal to the value of the debt represents the cost of eliminating credit risk. Choice 'b' is the correct answer.

Note that it is improbable that a put on the firm's assets is available in real life to debt holders. However, the same effect can be synthetically achieved by using the shares of the firm as a proxy for its assets, and shorting an appropriate number of shares. Such a synthetic put will require frequent readjustments.

Which of the following is not a risk faced by a bank from holding a portfolio of residential mortgages?

Choice 'd' represents a risk that does not arise from its holdings of mortgages. Therefore Choice 'd' is the correct answer.

All the other risks identified are correct - the bank faces interest rate, default and prepayment risks on its mortgages.

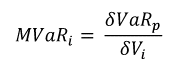

Which of the following best describes the concept of marginal VaR of an asset in a portfolio:

The correct answer is choice 'd'

Marginal VaR is just the change in total VaR from a $1 change in the value of the asset in the portfolio. All other answers are incorrect. Mathematically, it is expressed as follows, where VaRp is the VaR for the portfolio, and Vi is the value of the asset in question.

Other answers describe other VaR related concepts such as incremental VaR, Component VaR and Conditional VaR.