The CIMAPRO19-P02-1 exam, also known as P2 Advanced Management Accounting, is a core component of the CIMA Professional Qualification. It assesses your ability to apply management accounting techniques to real-world business scenarios, including cost management, investment decisions, and organizational performance control. This page provides a structured overview of the exam content, question formats, and practical preparation strategies to help you build confidence and achieve your target score.

Use this topic map to guide your study for CIMA CIMAPRO19-P02-1 (P2 Advanced Management Accounting) within the CIMA Professional Qualification path.

CIMAPRO19-P02-1 combines multiple-choice questions with scenario-based items to assess both technical knowledge and professional judgment. The exam measures your ability to apply management accounting concepts to complex, multi-faceted business situations.

Questions progress in difficulty and require you to justify your reasoning, moving beyond memorization to demonstrate professional competence in management accounting practice.

A structured study plan that maps topics to weekly learning goals, combined with regular practice and review, builds both knowledge depth and exam confidence. Allocate time proportionally to topic weight and your own knowledge gaps, ensuring you understand connections between cost management, investment decisions, and performance control.

Explore other CIMA certifications: view all CIMA exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to CIMAPRO19-P02-1 and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test, or get a Bundle Discount offer for both formats: P2 Advanced Management Accounting.

Capital Investment Decision Making and Managing and Controlling the Performance of Organisational Units typically account for a significant portion of the exam. However, all five domains are important; the exam often combines them in integrated scenarios, so balanced preparation across all topics is essential.

Cost allocation decisions directly influence investment appraisal outcomes and performance measurement. For example, how you assign overhead to products affects the profitability analysis used in capital budgeting, and the metrics you choose for performance evaluation should align with the organization's investment strategy. Understanding these linkages helps you answer integrated scenario questions effectively.

Candidates often confuse costing methods or miscalculate time value of money in investment scenarios. Others fail to consider qualitative factors alongside quantitative analysis, or miss the strategic context required for performance measurement recommendations. Read questions carefully, show your working, and always explain your reasoning with reference to the business scenario.

Start by identifying the type of variance (material, labor, overhead, or sales) and the relevant standard or budget. Calculate the variance accurately, then interpret what it tells you about operational performance. Always consider root causes and link your analysis to the broader control environment and organizational objectives outlined in the scenario.

Focus on high-weight topics and complete at least one full-length practice mock under timed conditions. Review your performance by domain, re-study any weak areas using your notes and explanations, and work through a few integrated case scenarios. Avoid cramming new material; instead, consolidate and refine your understanding of core concepts you have already covered.

A supermarket group has experienced operational problems during recent years, including a shortage of warehousing space due to increasing turnover and poor inventory management. The product portfolio has expanded considerably. Although this has led to increased sales volume, marketing and logistics costs have increased disproportionately. Non product-specific costs have also increased significantly.

Management is now considering using Direct Product Profitability (DPP).

Which of the following statements are valid in respect of the possible implementation of DPP within the supermarket group?

Select ALL that apply.

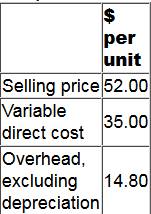

A company is considering investing $680,000 in a machine to manufacture a new product. A consultant has been appointed to advise on the investment and the company is committed to paying $10,000 to the consultant in year 1, even if the project does not go ahead.

300,000 units of the new product will be produced and sold each year. Unit cost and revenue information based on this level of output is as follows.

60% of the overhead cost is variable. Of the remainder, 10% consists of allocated head office overheads.

The selling price will increase by 2% each year in line with inflation, beginning in year 2. Fixed price contracts mean that all unit costs will remain unaltered.

Taxation information:

* 100% first year allowance will be available for the purchase of the machinery.

* The taxation rate is 30% of taxable profits, payable in the year after that in which the liability arises.

For the purpose of deciding whether to proceed with the investment, what is the relevant cash flow in year 2?

Which of the following statements about modified internal rate of return (MIRR) and internal rate of return (IRR) is correct?

A company expects to sell 3,600 units of Product A at a selling price of $750 per unit during the forthcoming year. The currently expected variable cost per unit is $860 per unit. The company requires a return of 15% during the forthcoming year on its investment of $2.4 million in Product

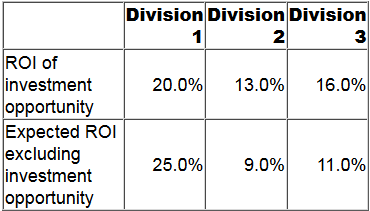

A company has three divisions, each of which is an investment centre. The divisional managers' performance is assessed using return on investment (ROI). A higher ROI will result in a higher bonus for the divisional manager.

The company's cost of capital is 15%.

For the forthcoming year each divisional manager has one investment opportunity available as follows:

The manager(s) of which division(s) will proceed with their respective investment opportunity?