The CIMAPRO19-P01-1 exam, formally known as P1 Management Accounting, is a foundational qualification within the CIMA Professional Qualification pathway. It assesses your ability to apply core management accounting principles, analyze financial data, and support business decision-making. This page provides a structured overview of the syllabus, question formats, and practical preparation strategies to help you study efficiently and perform confidently on exam day.

Use this topic map to guide your study for CIMA CIMAPRO19-P01-1 (P1 Management Accounting) within the CIMA Professional Qualification path.

CIMAPRO19-P01-1 combines multiple-choice and scenario-based questions to assess both theoretical knowledge and practical reasoning. The exam measures your ability to recall key concepts, apply them to realistic business situations, and justify your conclusions.

Questions progress in difficulty, starting with straightforward recall and moving toward integration of multiple concepts. Success depends on understanding not just "what" but "why" accounting choices matter in practice.

An effective study plan spreads learning across 8-12 weeks, allocating focused time to each topic cluster and building connections between concepts. Combine reading, worked examples, and practice questions to reinforce understanding and build exam confidence.

Explore other CIMA certifications: view all CIMA exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to CIMAPRO19-P01-1 and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test or get Bundle Discount offer for both Formats: P1 Management Accounting.

Standard costing, variance analysis, and budgeting are core pillars of P1 Management Accounting and usually account for 40-50% of exam content. Cost accounting systems and responsibility centres also feature prominently. Allocate study time proportionally, ensuring you master variance calculations and budget preparation thoroughly.

Cost accounting systems determine how costs are collected and assigned to products; standard costing then uses those cost classifications to set performance benchmarks. In practice, a company might use absorption costing to value inventory (financial reporting) while also maintaining standard costs for internal control and variance analysis. Understanding both systems and their interplay is essential for effective management decision-making.

Candidates often confuse cost classifications (fixed vs. variable, direct vs. indirect) or misinterpret variance signs (favorable vs. unfavorable). Another frequent error is failing to link variance analysis back to root causes or management actions. Weak transfer pricing justifications and incomplete budget narratives also cost marks. Practice explaining your reasoning in full sentences, not just numbers.

Review your summary notes and formula sheets daily, but avoid cramming new material. Spend 60% of time on full-length timed practice tests and 40% on targeted review of weak topics. Time yourself strictly to build pacing confidence. On the day before the exam, do light revision only and ensure you are well-rested.

No specific software experience is required for the exam. However, familiarity with spreadsheet modeling (Excel) and basic accounting system concepts helps you understand cost allocation and variance reporting in context. If you have access to a costing or ERP system, exploring how variances are calculated and reported will deepen your practical understanding.

A company manufactures two products and has two production constraints.

When the graphical approach to linear programming is used, the axes of the graph will show:

A medium-sized manufacturing company, which operates in the electronics industry, has employed a firm of consultants to carry out a review of the company's planning and control systems. The company presently uses a traditional incremental budgeting system and the inventory management system is based on economic order quantities (EOQ) and reorder levels. The company's normal production patterns have changed significantly over the previous few years as a result of increasing demand for customized products. This has resulted in shorter production runs and difficulties with production and resource planning. The consultants have recommended the implementation of activity based budgeting and a manufacturing resource planning system to improve planning and resource management.

What are the benefits for the company that could occur following the introduction of an activity based budgeting system?

Select ALL the correct answers.

References:

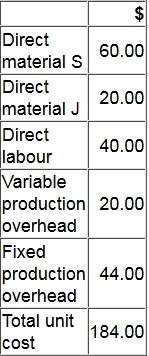

The cost card for one unit of Product G is as follows:

The opening and closing inventories of Product G for month 5 are budgeted to be 10 units and 60 units respectively.

Profit for month 5 using absorption costing is budgeted to be $15,000.

What is the budgeted profit for month 5 using throughput costing?

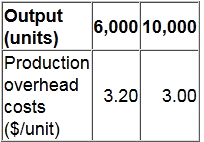

The following details are available for a company's production overhead costs at different levels of activity:

The company uses the high-low method to calculate its budgeted production overhead costs.

What is the budget for production overhead costs at an activity level of 8,500 units?

Give your answer as a whole number.