The CIMAPRA19-F02-1 exam (F2 Advanced Financial Reporting) is a core component of the CIMA Professional Qualification, designed for finance professionals who need to master complex financial reporting standards and group accounting principles. This exam validates your ability to interpret, prepare, and analyse advanced financial statements in real-world business contexts. Whether you are progressing through the CIMA pathway or strengthening your technical reporting expertise, this page provides a clear roadmap of the syllabus, question formats, and effective preparation strategies. Use the resources and guidance below to build confidence and achieve a strong result.

Use this topic map to guide your study for CIMA CIMAPRA19-F02-1 (F2 Advanced Financial Reporting) within the CIMA Professional Qualification path.

The CIMAPRA19-F02-1 exam employs a mix of question types that assess both theoretical knowledge and practical application of financial reporting principles in realistic business situations.

Questions progress in difficulty and emphasise real-world application, ensuring candidates can not only recall standards but also navigate ambiguity and justify decisions under pressure.

An efficient study routine maps the six core topics to a structured timeline, balances concept learning with practice, and builds confidence through progressive testing. Allocate 4-6 weeks to cover all areas, with emphasis on group accounts and financial reporting standards, which typically carry the greatest weight.

Explore other CIMA certifications: view all CIMA exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to CIMAPRA19-F02-1 and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test, or get a Bundle Discount offer for both formats: F2 Advanced Financial Reporting.

Financial Reporting Standards and Group Accounts typically account for 40-50% of the exam content. These topics are foundational to all other areas and require deep understanding rather than surface knowledge. Financing Capital Projects and Analysing Financial Statements also feature prominently, so allocate study time proportionally to these areas.

In a real business, a group company may lease assets (IFRS 16), which must be recognised on the balance sheet and consolidated into group accounts. The lease liability and right-of-use asset then affect group financial ratios and cash flow analysis. The exam tests your ability to trace these connections and understand how one accounting decision ripples through financial statements and performance metrics.

Frequent errors include misapplying consolidation elimination entries, overlooking non-controlling interests, and failing to distinguish between capitalisation and expensing of project costs. Many candidates also rush through scenario questions without fully reading the facts, leading to incorrect treatment selection. Taking time to identify all relevant standards and cross-check your working reduces these errors significantly.

While hands-on experience with accounting systems is valuable, the exam focuses on conceptual understanding and manual preparation of financial statements rather than software operation. Prioritise understanding the mechanics of consolidation, the logic of standard application, and the ability to construct journal entries and adjustments. Familiarity with spreadsheet-based financial modelling and ratio calculation is more directly applicable.

In the final week, avoid learning new material; instead, focus on revision questions, review your practice test results, and work through any topics where your scores were inconsistent. Complete one final timed mock to maintain pacing confidence. Spend time reviewing standard definitions, consolidation elimination entries, and common ratio formulas so they are fresh in your memory on exam day.

Which TWO of the following are relevant ethical considerations when selecting an accounting policy?

What figure will be presented inGHI's consolidated statement of changes in equity for the year ended 31 December 20X4, in respect ofdividends paidtonon-controlling interest?

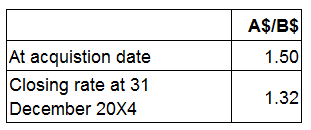

A group presents its financial statements in A$.

The goodwill of its only foreign subsidiary was measured at B$100,000 at acquisition. There have been no impairments to this goodwill.

Exchange rates (where A$/B$ is the number of B$'s to each A$) are as follows:

The value of goodwill to be included in the group's statement of financial position in respect of its foreign subsidiary for the year ended 31 December 20X4 is:

HJ is currently in dispute with an employee, who is claiming $400,000 in a legal case against them.

HJ's legal advisors have stated that it is probable that they willlose the case and will have to pay the amount claimed.

Also, HJ areclaiming $250,000 from a supplierof defective goods and the legal advisors have stated that it is probable that HJ will besuccessful in this claim.

What is the correct accounting treatment for these two items in HJ'sfinancial statements?

Which TWO of the following are true for an entity raising equity finance using a rights issue rather than a placing of equity shares to new investors?