The CIMAPRA19-F01-1 exam, also known as F1 Financial Reporting, is a foundational assessment within the CIMA Professional Qualification pathway. It evaluates your ability to understand financial reporting frameworks, interpret financial statements, and apply taxation and cash management principles in real-world contexts. This page guides you through the syllabus, question formats, and effective study strategies to help you prepare confidently. Whether you are new to CIMA or building on prior knowledge, a structured approach to these core topics will strengthen your readiness for exam day.

Use this topic map to guide your study for CIMA CIMAPRA19-F01-1 (F1 Financial Reporting) within the CIMA Professional Qualification path.

CIMAPRA19-F01-1 uses a mix of question types to assess both conceptual understanding and practical application. The exam measures your ability to interpret data, make informed decisions, and communicate financial reasoning clearly.

Questions progress in difficulty and emphasize real-world application, moving from simple recall to complex judgment calls that reflect the decisions faced by finance professionals.

An effective study plan distributes effort across all topics, builds depth through repeated practice, and includes regular self-assessment. Allocate 4-6 weeks to cover the syllabus thoroughly, with increasing focus on weak areas as you progress.

Explore other CIMA certifications: view all CIMA exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to CIMAPRA19-F01-1 and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test, or get a Bundle Discount offer for both formats: F1 Financial Reporting.

Financial Statements and Working Capital management tend to be heavily tested because they directly apply to real-world finance roles. Regulatory Environment and Taxation also appear frequently, but often in combination with statement analysis or cash management scenarios. Revision topics reinforce connections across all areas, so mastering the core topics first ensures you are prepared for any combination the exam presents.

In practice, these topics work together: regulatory requirements shape how you prepare financial statements, tax planning decisions affect cash flow, and working capital management is reflected in the statement of financial position and cash flow statement. Understanding these links helps you answer scenario questions more effectively because you can see why a particular decision matters across multiple areas. For example, a change in inventory policy affects both working capital ratios and tax deductions, so candidates who see these connections answer more confidently.

Many candidates focus too heavily on memorizing definitions and neglect scenario practice, then struggle when questions require analysis rather than recall. Others miscalculate working capital metrics or miss the tax implications of business decisions. A third common error is rushing through calculation questions without double-checking units or rounding. Review your practice test results carefully to spot your own patterns, then allocate extra study time to those weak areas before exam day.

In the final week, move away from learning new content and focus on consolidation and speed. Review your lowest-scoring topic areas from practice tests, do a quick refresher on key formulas and definitions, and complete one final timed mock exam. Use this mock to practice pacing and identify any remaining gaps. On the day before the exam, do light review only and ensure you are well-rested; cramming new material at this stage typically increases anxiety without improving performance.

No, the exam does not require hands-on software experience. However, familiarity with how financial statements are generated and how data flows through accounting systems can help you understand concepts more deeply. If you have access to accounting software or sample datasets, working through simple exercises like preparing a cash flow forecast or calculating working capital ratios can reinforce your learning. The exam itself focuses on conceptual understanding and analysis, not software navigation.

The International Accounting Standards Board's "The Conceptual Framework for Financial Reporting" identifies fundamental and enhancing qualitative characteristics of financial statements.

Which of the following is included within the fundamental characteristics?

WX is considering an investment in ST.

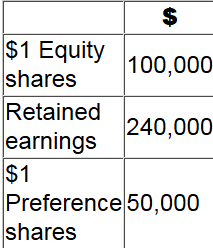

At 31 December 20X2 ST had the following balances in its statement of financial position:

Which of the following would cause ST to become an associate investment of WX?

Mr K is being pressured by his manager to change figures in his report so that it will improve his manager's bonus.

His manager has promised Mr K a promotion if he agrees to do this.

What threats is Mr K facing?

An entity has an inventory holding period of 52 days.

This means that the inventory:

UV's financial statements for the year ended 31 March 20X8 were approved for publication on 30 June 20X8.

In accordance with IAS 10 Events After the Reporting Period, which of the following material events would have been classified as a non-adjusting event in these financial statements?