The CIMAPRA17-BA3-1 exam, also known as BA3 - Fundamentals of Financial Accounting, is a core component of the CIMA Certificate in Business Accounting. This exam validates your ability to understand and apply foundational accounting principles, record transactions accurately, prepare financial statements, and analyze financial performance. Whether you're beginning your accounting career or transitioning into finance, this page provides a structured study roadmap to help you prepare effectively and confidently approach the exam.

Use this topic map to guide your study for CIMA CIMAPRA17-BA3-1 (BA3 - Fundamentals of Financial Accounting) within the CIMA Certificate in Business Accounting path.

The CIMAPRA17-BA3-1 exam uses a mix of question types to assess both theoretical knowledge and practical application of accounting concepts. Questions progress in difficulty and reflect real-world scenarios you will encounter in finance roles.

Questions are designed to simulate the reasoning and judgment required in accounting practice, with difficulty increasing as you progress through the exam.

A structured study plan mapped to the syllabus topics helps you build knowledge progressively and identify weak areas early. Allocate time proportionally to each domain, practice with realistic questions, and conduct timed reviews to build confidence and pacing.

Explore other CIMA certifications: view all CIMA exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to CIMAPRA17-BA3-1 and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test, or get a Bundle Discount offer for both formats: BA3 - Fundamentals of Financial Accounting.

Recording Accounting Transactions and Preparation of Accounts for Single Entities typically represent the largest portion of the exam, as these topics test core procedural skills. However, all four domains are essential; Accounting Principles provide the foundation for correct treatment, and Analysis of Financial Statements is increasingly important as you progress through the CIMA Certificate in Business Accounting.

Accounting Principles guide how you record transactions (domain B), which then flow into account preparation and adjustments (domain C). The resulting financial statements are then analyzed using ratios and trends (domain D) to assess business performance. Understanding these connections helps you see why a principle matters and how a transaction ultimately affects financial analysis.

Frequent errors include incorrect journal entries due to misunderstanding debit/credit rules, missing or miscalculating year-end adjustments, and misinterpreting which figures to use in ratio calculations. Many candidates also rush through scenario questions without reading all details, leading to wrong treatment choices. Careful reading, double-checking entries, and verifying adjustment calculations significantly reduce these errors.

Hands-on experience with bookkeeping or accounting software is valuable but not essential; the exam tests conceptual understanding and standard procedures rather than specific software. If you have access to practice, focus on manual journal entries, trial balance reconciliation, and financial statement preparation. If not, thorough study of worked examples and practice questions will build the same competency.

Focus on weak areas identified in practice tests rather than re-studying strong topics. Create a one-page summary of key definitions, adjustment types, and ratio formulas. Do a final timed practice test to confirm pacing and build confidence. Avoid learning new material; instead, reinforce what you already know and ensure you can execute calculations quickly and accurately under time pressure.

Where a transaction is credited to the correct ledger account but debited to the heat and light account instead of the rent and rates account, the error is known as an error of:

MNO operates an imprest system to maintain a float of petty cash of 5100 At the end of the week the petty cash expense vouchers total $76 and there is $36 cash in the float. Which of the following, taken independently, would explain this difference of $10?

Below is some information about Company TYY:

TYY offers a wholesale price for Product P of 650 per 100 quantity.

TYY offers regular customers a 35% trade discount.

On every 15th of the month, TYY offers a 15% cash discount on sales.

MPU wants to make a purchase from TTY for the first time, of900 Product Ps on the 15th of June. How much will MPU pay for this purchase?

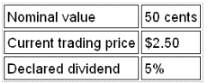

Refer to the exhibit.

The following information is available about the ordinary shares of a public limited company:

A shareholder who purchased 20,000 shares at a price of $1.90 will receive a dividend of