The CIMAPRA17-BA2-1 exam, also known as BA2 - Fundamentals of Management Accounting, is a core component of the CIMA Certificate in Business Accounting. It validates your ability to understand and apply foundational management accounting principles in real business contexts. This exam assesses both theoretical knowledge and practical decision-making skills across costing, planning, control, and strategic analysis. This page provides a clear roadmap of the syllabus, question formats, and effective study strategies to help you prepare confidently.

Use this topic map to guide your study for CIMA CIMAPRA17-BA2-1 (BA2 - Fundamentals of Management Accounting) within the CIMA Certificate in Business Accounting path.

The CIMAPRA17-BA2-1 exam uses a variety of question types designed to test both conceptual understanding and practical application of management accounting principles. Questions progress in difficulty and require candidates to apply knowledge to realistic business scenarios.

Questions increase in complexity as you progress, moving from isolated knowledge checks to integrated scenarios that demand critical thinking and multi-step reasoning.

Effective preparation requires a structured approach that maps each syllabus topic to dedicated study time and reinforces connections between costing, planning, control, and decision-making. A systematic routine helps you build confidence and identify weak areas early.

Explore other CIMA certifications: view all CIMA exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to CIMAPRA17-BA2-1 and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test, or get a Bundle Discount offer for both formats: BA2 - Fundamentals of Management Accounting.

Costing (Topic B) and Planning and Control (Topic C) together account for the majority of exam questions, as they form the operational core of management accounting. Decision Making (Topic D) is heavily tested through scenario-based items that integrate costing and control concepts. Topic A provides essential context but typically appears in fewer standalone questions; however, understanding it strengthens your ability to answer questions across all other areas.

In practice, management accountants first understand the organizational context (Topic A), then design costing systems (Topic B) to capture accurate cost information. This data feeds into budgets and performance monitoring (Topic C), which are used to support strategic and operational decisions (Topic D). For example, a costing decision about whether to use absorption or marginal costing directly affects budget preparation and variance analysis, which in turn informs pricing and product mix decisions. Recognizing these connections helps you answer integrated case study questions effectively.

Candidates often confuse absorption and marginal costing methods, particularly when calculating inventory values and profit under each approach. Another frequent error is misinterpreting variance analysis results without considering the underlying operational causes. Many also rush through scenario questions without identifying relevant costs, leading to poor decision recommendations. Finally, some candidates neglect to link budget variances back to the costing system or operational performance, missing opportunities to demonstrate integrated thinking.

In your final week, focus on reviewing weak areas identified in your mock exam rather than re-studying entire topics. Complete one more timed practice test to maintain pacing discipline and boost confidence. Spend time on scenario-based questions, as these require the most integrated thinking and are often the highest-value items. Avoid learning new material; instead, consolidate your understanding by working through explanations of difficult questions and ensuring you can articulate the reasoning behind correct answers.

While the exam does not require knowledge of specific accounting software, practical experience with costing calculations, budget preparation, or variance analysis significantly strengthens your understanding. If you have access to spreadsheet exercises or real cost data, working through practical scenarios helps you grasp how management accounting concepts apply in business. However, the exam focuses on principles and decision-making rather than system navigation, so strong conceptual knowledge and practice questions are your primary study tools.

An increase in variable costs per unit, where selling price and fixed costs remain constant, will result in which of the following:

In a manufacturing company which produces a range of products, the cost of a royalty payment made to the product designer would be classified as A.

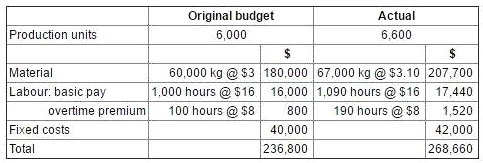

The budget and actual cost statements for the production department for the latest period were as follows.

Notes.

The 10% increase in production was required to meet unexpected additional sales demand.

The production manager is responsible for negotiating the price of materials with suppliers.

The normal working time is 900 hours per period. Any overtime worked above these 900 hours is paid at a premium of 50%.

In preparing the flexible budget for the latest period, which TWO of the following statements are correct? (Choose two.)

Refer to the exhibit.

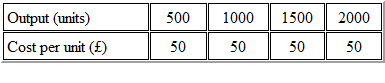

Which type of cost do the following figures represent?

The staffing policy for a supermarket is to have one cashier station open for every forecasted 20 customers per hour. Cashiers are hired by the hour as and when required, and do not perform any other duties.

The cost of the cashiers in relation to the number of customers would be classified as which type of cost?