The Fundamental Payroll Certification Exam (FPC-Remote) validates your competency in core payroll operations and compliance. Offered by the American Payroll Association (APA), this certification is designed for payroll professionals seeking to demonstrate mastery of essential payroll functions in a remote-friendly format. This page provides a clear roadmap of exam topics, question formats, and practical preparation strategies to help you succeed.

Use this topic map to guide your study for APA FPC-Remote (Fundamental Payroll Certification Exam) within the Fundamental Payroll path.

The FPC-Remote exam uses multiple-choice and scenario-based questions to assess both conceptual knowledge and applied judgment. Questions progress in difficulty and reflect real payroll situations you will encounter.

The exam balances foundational knowledge with practical reasoning, ensuring that certified professionals can handle both routine tasks and complex payroll challenges.

An effective study plan allocates time proportionally to exam topics and builds confidence through repeated practice. Start by mapping each topic to weekly study blocks, then reinforce learning with practice questions and scenario reviews.

Explore other APA certifications: view all APA exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to FPC-Remote and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test, or get a Bundle Discount offer for both formats: Fundamental Payroll Certification Exam.

Calculation of the Paycheck and Compliance / Research and Resources typically represent the largest portion of the exam. These areas directly impact payroll accuracy and legal compliance, so allocate study time accordingly. However, all seven topics are tested, so maintain balanced preparation across the full syllabus.

In practice, Core Payroll Concepts and Payroll Process and Supporting Systems form the foundation of daily operations. Compliance requirements shape how you handle deductions and withholding, while Accounting ensures payroll data flows correctly to financial records. Understanding these connections helps you see why each topic matters and improves retention.

Direct experience with payroll software, tax form completion, and reconciliation procedures is valuable. If you lack hands-on exposure, focus on scenario-based practice questions and study real payroll examples. Understanding how systems validate data and how calculations work in practice will strengthen your ability to answer applied questions.

Frequent errors include misunderstanding overtime rules, confusing federal and state tax treatment of benefits, and overlooking reconciliation steps. Many candidates also rush through calculation items without double-checking work. Slow down on computation questions, reread compliance scenarios carefully, and verify your logic against the regulations cited.

Reduce new material intake and focus on timed practice tests and weak-area review. Take at least one full-length mock exam under realistic conditions to identify pacing issues. In the days before the exam, review high-stakes topics like tax withholding and audit procedures, then rest well the night before to enter the exam alert and confident.

The due date for filing Form 941 is the:

Form 941 is due on the last day of the month following the end of the quarter.

Example:

Q1 (Jan--Mar) due: April 30

Q2 (Apr--Jun) due: July 31

IRS Form 941 Instructions

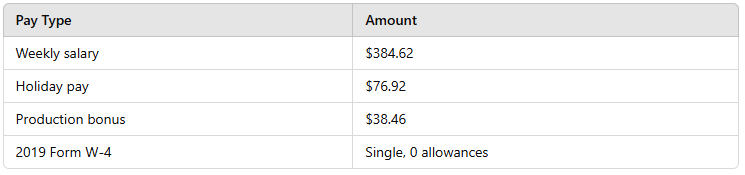

Using the percentage method for automated payroll systems, calculate the federal income tax withholding based on the following information:

Total taxable wages: $384.62 + $76.92 + $38.46 = $500.00

Using IRS percentage method tables, withholding = $39.04

IRS Publication 15-T (Tax Withholding Tables)

Which of the following documents listed on Form I-9 can be used to establish both an employee's identity and employment eligibility?

Comprehensive and Detailed Explanation:

According to Form I-9, Employment Eligibility Verification, an unexpired U.S. passport is a List A document that establishes both an employee's identity and work authorization.

A Social Security card (Option A) is a List C document, which only proves employment authorization but not identity.

A Voter's Registration Card (Option C) is not an acceptable I-9 document for identity or work authorization.

A Driver's License (Option D) is a List B document, which only proves identity but not employment eligibility.

An upgrade to a payroll system can impact all of the following documentation within the payroll department EXCEPT:

Comprehensive and Detailed Explanation:

A payroll system upgrade affects documentation related to payroll processing but does not change union contracts.

Option A (User manuals): Correct -- New system features require updated manuals for payroll staff.

Option C (Business continuity plans): Correct -- System changes must be included in disaster recovery plans.

Option D (Standard operating procedures -- SOPs): Correct -- Payroll procedures need updates for new workflows.

However, union contracts (Option B) remain unchanged unless a new agreement is negotiated.

Payroll.org -- Payroll System Implementation Best Practices

IRS -- Payroll System Compliance Requirements

Payroll standard operating procedures should be updated no less frequently than:

Comprehensive and Detailed Explanation:

Payroll Standard Operating Procedures (SOPs) must be regularly updated to maintain compliance and accuracy.

Best practice is to update SOPs whenever workflows change (Option C).

Option A (Annually) is incorrect because waiting a full year could lead to outdated procedures.

Option B (Quarterly) is incorrect unless payroll processes are highly dynamic.

Option D (When management changes) is incorrect because processes may change independently of leadership changes.

Payroll.org -- Payroll Policies and Procedures Best Practices

IRS -- Payroll Compliance Guidelines