The Certified Credit Research Analyst - Level 2 (CCRA-L2) exam, offered by AIWMI, validates your ability to analyze credit risk, manage portfolios, and apply regulatory frameworks in banking and financial institutions. This exam is designed for credit professionals, analysts, and managers who need to demonstrate advanced competency in credit research and decision-making. This page guides you through the syllabus, question formats, and effective preparation strategies to help you pass with confidence.

Use this topic map to guide your study for AIWMI CCRA-L2 (Certified Credit Research Analyst - Level 2) within the Certified Credit Research Analyst path.

The CCRA-L2 exam combines knowledge-based and scenario-driven questions to assess both theoretical understanding and practical judgment in credit analysis and risk management.

Questions progress in difficulty and emphasize practical application, reflecting the judgment required in live credit environments.

An organized study plan aligned to the five modules ensures you build knowledge progressively and reinforce connections between credit strategy, monitoring, and risk management. Dedicate 4-6 weeks to balanced coverage, with extra time for quantitative topics and case analysis.

Explore other AIWMI certifications: view all AIWMI exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to CCRA-L2 and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test, or get Bundle Discount offer for both formats: Certified Credit Research Analyst - Level 2.

Credit Risk Models and Regulations and Credit Monitoring with NPA Management typically account for 30-40% of the exam. However, all five modules are important; a balanced study approach ensures you are not caught off-guard by scenario questions that blend multiple topics.

In practice, internal credit ratings inform which borrowers you accept into the portfolio and at what pricing. Ongoing monitoring uses those same rating criteria to detect deterioration early, triggering NPA management actions or portfolio rebalancing. Understanding this workflow helps you answer integrated case questions correctly.

Many candidates focus too heavily on memorizing regulatory ratios and miss the practical judgment required in scenario questions. The exam tests whether you can apply concepts to real credit decisions, not just recall definitions. Practice case-based questions and explain your reasoning to build this skill.

Candidates with 2+ years in credit analysis, relationship management, or risk roles typically find the exam more intuitive. If you lack direct experience, prioritize understanding how different facility types work (term loans vs. working capital), how to read financial statements for repayment capacity, and how regulatory capital rules affect lending decisions.

In the final week, take one full-length timed practice test to identify remaining weak spots, then review explanations and revisit those specific topics. Avoid re-reading entire modules; instead, focus on clarifying concepts you struggle with and practicing similar question types until they feel familiar.

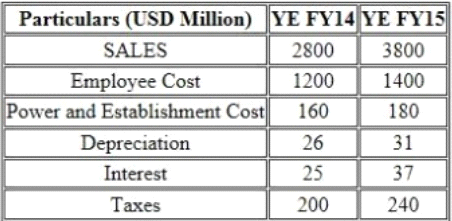

Based on the common size statement analysis which of the following statement regarding employee cost is correct?

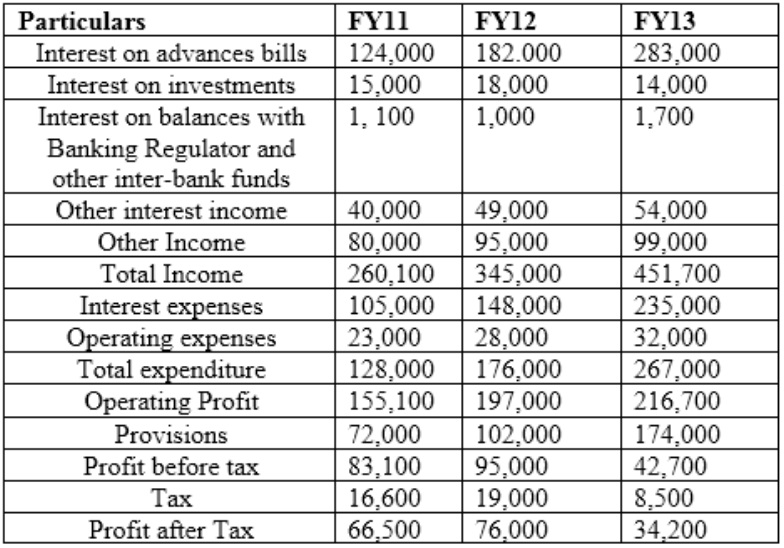

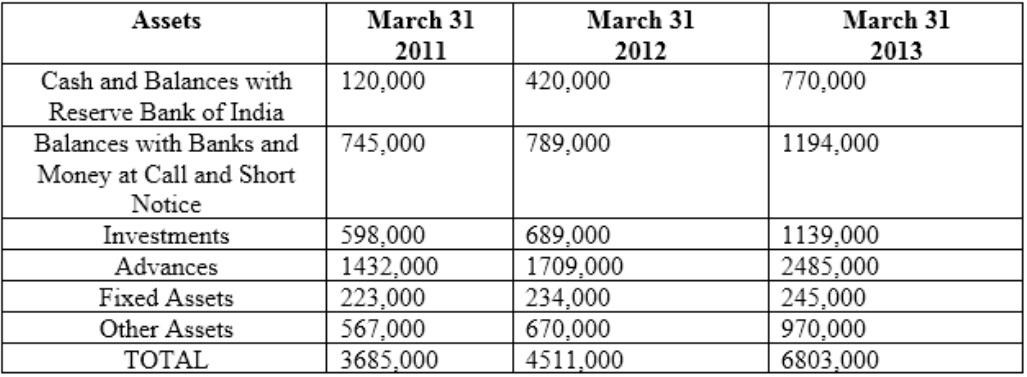

Following is information related banks:

Auckland Ltd is a public sector bank operating with about 120 branches across Indi

a. The bank has been in business since 1971 and has about 40% branches in rural areas and about 75% of all branches are in

Western India. On the basis of the size, Auckland Ltd will be ranked at number 31 amongst 40 banks in India.

Although top management has appointment period of 5 years, generally they retire on ach sieving age of 60 years with an average tenure of only 2 years at the top job.

Profit and Loss Account

Balance Sheet

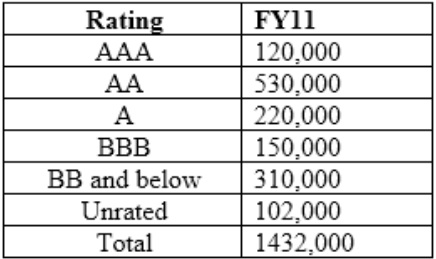

The rating wise break-up of assets for FY11 is as follows:

Computer risk weighted assets for Auckland Ltd for FY11:

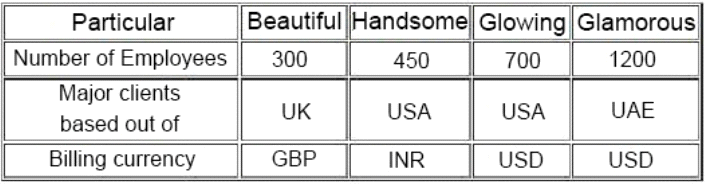

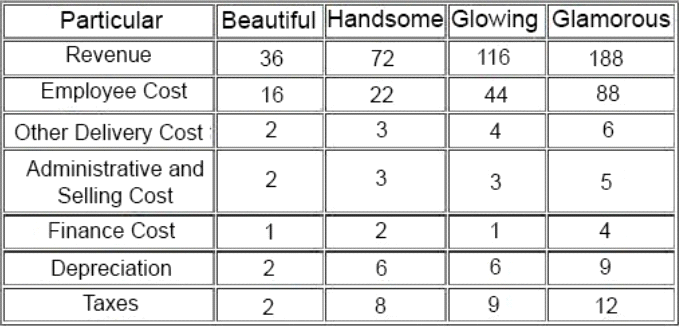

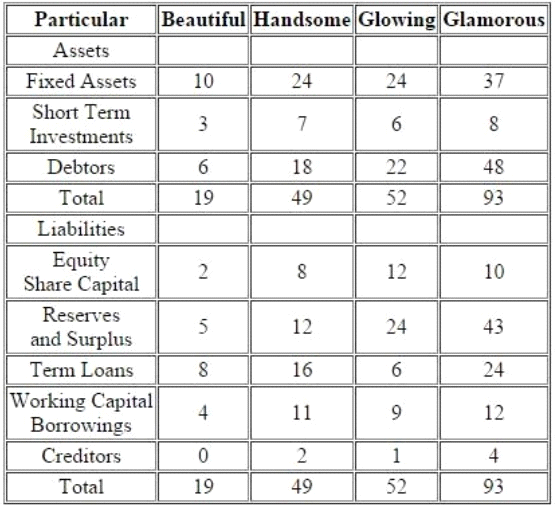

''Following four entities operate in the Indian IT and BPO space. They all are into same segment of providing off-shore analytical services. They all operate on the labour cost-arbitrage in India and the countries of their clients. Following information pertains for the year ended March 31, 2013.

The year FY13, was typically a good year for Indian IT companies. For FY14, the economic analysts have given following predictions about the IT Industry:

A) It is expected that INR will appreciate sharply against other USD.

B) Given high inflation and attrition in IT Industry in India, the wages of IT sector employees will increase more sharply than Inflation and general wage rise in country.

C) US Congress will be passing a bill which restricts the outsourcing to third world countries like India.

While analyzing the four entities, you come across following findings related to Glowing:

Glowing is promoted by Mr.M R Bhutta, who has earlier promoted two other business ventures, He started with ABC Entertainment Ltd in 1996 and was promoter and MD of the company. ABC was a listed entity and its share price had sharp movements at the time of stock market scam in late 1990s. In 1999, Mr. Bhutta sold his entire stake and resigned from the post of MD. The stock price declined by about 90% in coming days and

has never recovered. Later on in 2003, Mr. Bhutta again promoted a new business, Klear Publications Ltd (KCL) an in the business of magazine publication. The entity had come out with a successful IPO and raised money from public. Thereafter it ran into troubles and reported losses. In 2009, Mr. Bhutta went on to exit this business as well by selling stake to other promoter(s). There have been reports in both instances with allegations that promoters have siphoned off money from listed entities to other group entities, however, nothing has been proved in any court.''

Which entity is best in terms of overall gearing ratio and net gearing ratio respectively: