The CPA-Regulation exam, administered by the AICPA, is a critical component of the Certified Public Accountant certification path. It evaluates your mastery of professional ethics, business law, and federal taxation across multiple contexts. This exam tests both foundational knowledge and the ability to apply concepts to real-world scenarios. Whether you are preparing for your first attempt or a retake, this page provides a clear roadmap of what to study and how to approach your preparation efficiently.

Use this topic map to guide your study for AICPA CPA-Regulation (CPA Regulation) within the Certified Public Accountant path.

The CPA-Regulation exam uses multiple question types to assess both conceptual understanding and practical judgment. Each format targets specific cognitive levels, from recall to analysis and application in client situations.

Questions progress in difficulty, moving from straightforward rule application to complex scenarios that mirror advisory and compliance work you will encounter as a Certified Public Accountant.

An effective study plan breaks the five content areas into manageable weekly segments, balances conceptual review with question practice, and includes timed assessments to build confidence. Allocate more time to areas where you have less professional experience or weaker foundational knowledge.

Explore other AICPA certifications: view all AICPA exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to CPA-Regulation and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test or get Bundle Discount offer for both Formats: CPA Regulation.

Federal taxation topics (Areas III, IV, and V) collectively represent the largest portion of the exam, reflecting the tax compliance and planning focus of the Regulation section. However, Area I (Ethics and Professional Responsibilities) and Area II (Business Law) are also heavily tested and essential for passing. Allocate study time proportionally, but do not neglect any area, as questions are distributed across all five domains.

Ethics and professional responsibility rules govern how you advise clients on tax matters and prepare returns, making Area I foundational to all other topics. Business law (Area II) underpins entity selection and structure decisions that drive tax planning in Areas IV and V. Understanding these connections helps you recognize when a tax strategy may create compliance or ethical concerns, which the exam tests through scenario-based questions.

Candidates often rush through scenario questions without fully reading all facts, leading to incorrect analysis. Misunderstanding the interplay between individual and entity-level taxation (Areas IV and V) is another frequent error. Additionally, overlooking procedural requirements in Area I, such as engagement letter requirements or tax return filing deadlines, costs points. Slow down on scenario items, map facts to rules systematically, and review procedural details in your final study week.

Focus on review and pacing rather than learning new material. Complete one full-length timed practice test early in the week, review all explanations, and identify your weakest areas. Spend the remaining days drilling those weak topics with targeted questions and flashcards. On the final day, review ethics rules and common procedural pitfalls, then rest. Avoid cramming new content; confidence comes from reinforcing what you already know.

While hands-on experience is valuable, it is not required to pass. The exam tests conceptual knowledge and applied reasoning that can be developed through study materials and practice questions. If you lack professional tax experience, prioritize scenario-based questions and simulations to build practical judgment. Focus on understanding the "why" behind rules, not just memorizing them, so you can apply concepts to unfamiliar situations on test day.

Among which of the following related parties are losses from sales and exchanges not recognized for tax purposes?

Choice 'c' is correct. Losses from sales and exchanges are not recognized for tax purposes between grandfather and granddaughter.

Rule: Losses are disallowed on sales between related parties. 'Related' includes brothers and sisters, husband-wife, lineal descendants (father, son, grandfather), and entities that are more than 50% owned by individuals, corporations, trusts and/or partnerships.

Choices 'a', 'b', and 'd' are incorrect, because losses from sales and exchanges are recognized for all 'in-laws.'

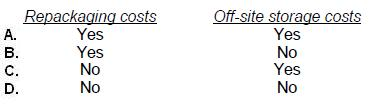

Under the uniform capitalization rules applicable to taxpayers with property acquired for resale, which of the following costs should be capitalized with respect to inventory if no exceptions have been met?

Choice 'a' is correct. Direct material, direct labor, and factory overhead (applicable indirect costs) are capitalized with respect to inventory under the uniform capitalization rules for property acquired for resale. Applicable indirect costs include depreciation and amortization, insurance, supervisory wages, utilities, spoilage and scrap, design expenses, repair and maintenance and rental of equipment and facilities (including offsite storage), some administrative costs, costs of bonus and other incentive plans, and indirect supplies and other materials (including repackaging costs).

Choices 'b', 'c', and 'd' are incorrect, per the above discussion.

Individual Taxation - Capital Gains and Losses

Cobb, an unmarried individual, had an adjusted gross income of $200,000 in 1990 before any IRA deduction, taxable social security benefits, or passive activity losses. Cobb incurred a loss of $30,000 in 1990 from rental real estate in which he actively participated. What amount of loss attributable to this rental real estate can be used in 1990 as an offset against income from nonpassive sources?

Choice 'a' is correct. Cobb may not use any of the loss attributable to his rental real estate as an offset against income from nonpassive sources in 1990 because he does not qualify for the 'Mom and Pop' exception. Under this exception, up to $25,000 of passive losses and the deduction equivalent of tax credits that are attributable to rental real estate may be used as an offset against income from nonpassive sources. This $25,000 allowance is reduced, but not below zero, by 50% of the amount by which the individual's modified AGI exceeds $100,000. The $25,000 is therefore completely phased out when modified AGI reaches $150,000. Because Cobb's AGI was $200,000, he did not qualify for the exception.

Choices 'b', 'c', and 'd' are incorrect. Rental activities are passive activities and generally are not allowed to use any of the loss attributable to the rental activity to offset any income produced from nonpassive sources. There is a limited exception in the case of losses from rental real estate in which the taxpayer actively participates, but Cobb did not qualify for it.

Tom and Joan Moore, both CPAs, filed a joint 1994 federal income tax return showing $70,000 in taxable income. During 1994, Tom's daughter Laura, age 16, resided with Tom. Laura had no income of her own and was Tom's dependent.

Determine the amount of income or loss, if any that should be included on page one of the Moores' 1994 Form 1040.

Tom's 1994 wages were $53,000. In addition, Tom's employer provided group-term life insurance on Tom's life in excess of $50,000. The value of such excess coverage was $2,000.

'N' is correct. $55,000. The value of employer-provided group term life insurance for which the face amount exceeds $50,000 is taxable income to the insured employee and the $53,000 in wages would both be included on page one, Form 1040.

Don Wolf became a general partner in Gata Associates on January 1, 1989, with a 5% interest in Gata's profits, losses, and capital. Gata is a distributor of auto parts. Wolf does not materially participate in the partnership business. For the year ended December 31, 1989, Gata had an operating loss of $100,000.

In addition, Gata earned interest of $20,000 on a temporary investment. Gata has kept the principal temporarily invested while awaiting delivery of equipment that is presently on order. The principal will be used to pay for this equipment. Wolf's passive loss for 1989 is:

Choice 'c' is correct. Wolf's passive loss for 1989 is $5,000 ($100,000 operating loss 5% interest in partnership).

Choice 'a' is incorrect. Wolf did not materially participate in the partnership, so the loss was passive.

Choice 'b' is incorrect. Wolf's passive loss of $5,000 could not be reduced by his distributive share of the partnership's 'interest income' totaling $1,000. Interest income is considered 'portfolio income,' and neither the partnership nor a partner can offset it against passive losses.

Choice 'd' is incorrect. No items of income or deduction from portfolio income or activities in which the taxpayer materially participates may be combined or offset with passive losses unless the activity generating the loss is completely disposed of in a taxable transaction.