The CPA-Financial exam, officially known as CPA Financial Accounting and Reporting, is a core component of the Certified Public Accountant credential pathway administered by the AICPA. This exam validates your ability to apply accounting principles, interpret financial statements, and make sound reporting decisions in real-world scenarios. Whether you're preparing for your first attempt or refining your study approach, this page provides a clear roadmap of exam content, question formats, and actionable preparation strategies. Use these resources to build confidence and ensure comprehensive coverage of all tested domains.

Use this topic map to guide your study for AICPA CPA-Financial (CPA Financial Accounting and Reporting) within the Certified Public Accountant path.

The CPA-Financial exam uses multiple question types to assess both conceptual knowledge and practical application. Questions progress in difficulty and require you to synthesize information across topics to solve realistic accounting challenges.

A structured study plan aligned to the four content areas ensures balanced preparation and reduces gaps in understanding. Dedicate time proportionally to each domain, with extra focus on Area II given its higher weight on the exam. Regular practice with varied question types builds both speed and accuracy.

Explore other AICPA certifications: view all AICPA exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to CPA-Financial and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test, or get a Bundle Discount offer for both formats: CPA Financial Accounting and Reporting.

Area II (Select Financial Statement Accounts) represents 30-40% of exam questions, making it the largest domain. Area I (Conceptual Framework) and Area III (Transactions) each represent significant portions, while Area IV (State and Local Governments) typically comprises a smaller but important segment. Allocate study time proportionally, but ensure you have solid foundational knowledge across all four areas.

Area I provides the conceptual foundation that underpins all accounting decisions. Area III (Transactions) describes the business events you encounter, which you then record and measure using the account treatments covered in Area II. These accounts roll up into financial statements that must comply with reporting standards outlined in Area I. For government entities, Area IV applies these principles under modified accrual accounting and fund-based reporting frameworks.

Many candidates rush through scenario-based items without carefully reading all facts, leading to incorrect conclusions about transaction classification or measurement. Others memorize journal entries without understanding the underlying standards, which causes errors when facts change slightly. Weak performance on Area IV often stems from insufficient exposure to governmental accounting rules. Avoid these pitfalls by reading questions thoroughly, studying standards rather than isolated examples, and dedicating focused time to less familiar topics.

In your final week, focus on review and pacing rather than learning new material. Take one or two full-length timed practice exams to simulate test conditions and identify any remaining speed or accuracy issues. Review detailed explanations for questions you missed, but avoid obsessing over borderline items. Maintain consistent sleep and study rhythm to stay sharp on exam day.

While practical accounting experience helps you understand real-world application and context, the exam tests your knowledge of standards and principles as defined by the AICPA and FASB. Candidates without extensive hands-on experience can succeed by thoroughly studying the conceptual framework, practicing varied question types, and working through scenario-based items that simulate workplace situations. Prioritize deep understanding of standards over reliance on experience alone.

According to the FASB conceptual framework, an entity's revenue may result from:

Rule: Revenues are inflows or other enhancements of assets and/or settlements (decreases) in liabilities resulting from the entity's ongoing major operations, not from 'incidental' operations.

Choice 'd' is correct. An entity's revenue may result from a decrease in a liability from primary operations.

Which of the following assumptions means that money is the common denominator of economic activity and provides an appropriate basis for accounting measurement and analysis?

Choice 'c' is correct. The monetary unit assumption means that money is the common denominator for economic activity and provides an appropriate basis for accounting measurements and analysis.

Choice 'a' is incorrect. The going concern assumption has nothing to do with money per se. The going concern assumption presumes that an entity will continue to operate in the foreseeable future.

Choice 'b' is incorrect. The periodicity has nothing to do with money per se. The periodicity assumption is that economic activity can be divided into meaningful time periods.

Choice 'd' is incorrect. The economic entity assumption has nothing to do with money per se. The economic entity assumption is that economic activity can be accounted for when considering an identifiable set of activities.

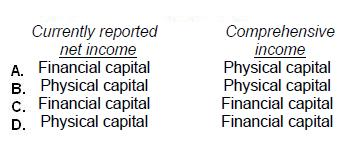

FASB's conceptual framework explains both financial and physical capital maintenance concepts. Which capital maintenance concept is applied to currently reported net income, and which is applied to comprehensive income?

Choice 'c' is correct. Financial capital - Financial capital.

Financial capital maintenance is considered to be an element of both 'currently reported net income' and 'comprehensive income.' This was a rare instance in which this type of information was asked on the exam.

According to the FASB conceptual framework, the usefulness of providing information in financial statements is subject to the constraint of:

Choice 'b' is correct. The pervasive constraint on providing information in financial statements is that the cost should be outweighed by the benefit to be derived from providing the information. SFAC 1 para. 23, SFAC 2 para. 133

Choice 'a' is incorrect. Consistency is an underlying concept for financial statements (and a secondary quality of accounting information), but it is not a constraint on providing information. SFAC 2 para. 120 Choice 'c' is incorrect. Reliability is a primary quality of accounting information and an underlying concept for financial statements, but it is not a constraint on providing information. SFAC 2 para. 58 Choice 'd' is incorrect. Representational faithfulness is an underlying concept for financial statements (as an element of reliability), but it is not a constraint on providing information. SFAC 2 para.

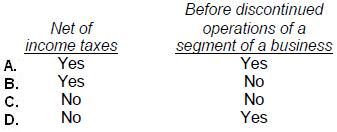

An extraordinary item should be reported separately on the income statement as a component of income:

Choice 'b' is correct, Yes - No. An extraordinary item should be reported separately on the income statement as a component of income:

Yes - net of income taxes.

No - after (not before) 'discontinued operations of a segment of a business.'