The CPA Auditing and Attestation exam, part of the Uniform CPA Examination administered by the AICPA, validates your ability to plan, execute, and report on audit and attestation engagements. This exam is designed for candidates who have completed their accounting education and are ready to demonstrate competency in professional auditing standards and practices. This page outlines the exam structure, core topics, question formats, and effective preparation strategies to help you study efficiently and build confidence before test day.

Use this topic map to guide your study for AICPA CPA-Auditing (CPA Auditing and Attestation) within the Uniform CPA Examination path.

The CPA Auditing and Attestation exam uses multiple-choice and scenario-based items to measure both foundational knowledge and applied reasoning. Questions progress in difficulty and require you to integrate concepts across the audit process.

Questions emphasize real-world application and expect you to connect planning decisions to execution and reporting outcomes.

Effective preparation combines structured topic review with progressive practice. Allocate study time proportionally to exam weight, and regularly link concepts across the four areas to reinforce how planning, execution, and reporting interconnect in actual audits.

Explore other AICPA certifications: view all AICPA exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to CPA-Auditing and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test, or get a Bundle Discount offer for both formats: CPA Auditing and Attestation.

Area III (Performing Further Procedures and Obtaining Evidence) and Area IV (Forming Conclusions and Reporting) typically account for a larger portion of exam questions because they test your ability to execute and conclude on audit work. However, all four areas are essential; a weakness in Area I or Area II will impact your ability to handle higher-order questions in Areas III and IV.

In practice, you begin with Area I principles to ensure independence and ethical conduct throughout the engagement. Area II risk assessment informs your audit strategy and procedure design. Area III execution involves gathering evidence based on your planned procedures. Area IV requires you to evaluate all evidence collected and form appropriate conclusions and reports. Understanding these connections helps you answer scenario questions that span multiple areas.

Direct experience with audit planning, fieldwork, and report preparation is highly beneficial. If you have limited hands-on experience, focus your study on understanding the purpose and execution of common procedures such as analytical procedures, substantive testing, and control testing. Practice questions with detailed explanations can bridge the gap by walking you through realistic scenarios and the reasoning behind audit decisions.

Candidates often confuse audit procedures with the risks they address, overlook the distinction between control testing and substantive procedures, and misinterpret audit report modifications. Another frequent error is failing to consider materiality and risk when evaluating evidence or determining the appropriate audit opinion. Careful reading of scenario details and linking your answer back to the specific facts presented will help you avoid these pitfalls.

In your final week, shift focus from new content to review and timed practice. Complete one full-length timed practice test to assess your pacing and identify any remaining knowledge gaps. Review explanations for incorrect answers and revisit those specific topics. Avoid cramming new material; instead, use this time to build confidence and reinforce your understanding of high-frequency topics and common question patterns.

Which of the following best describes the responsibility of the auditor to report significant deficiencies and material weaknesses in an attest engagement to examine the effectiveness of a nonissuer's internal control?

Choice 'a' is correct. In an attest engagement to examine the effectiveness of an entity's internal control, the auditor must communicate both significant deficiencies and material weaknesses to management and those charged with governance.

Choice 'b' is incorrect. The auditor is required to communicate significant deficiencies.

Choices 'c' and 'd' are incorrect. Both significant deficiencies and material weaknesses are required to be communicated to management and those charged with governance.

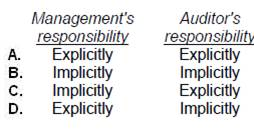

How are management's responsibility and the auditor's responsibility represented in the standard auditor's report?

Choice 'a' is correct. The responsibility of the auditor and the responsibility of management are stated explicitly in the introductory paragraph of the standard auditor's report.

Choices 'b', 'c', and 'd' are incorrect, as explained above.

An auditor's report would be designated a special report when it is issued in connection with:

Choice 'b' is correct. An auditor's report would be designated a special report when it is issued in connection with compliance with aspects of regulatory requirements related to audited financial statements.

Choice 'a' is incorrect. A 'review report' (not a 'special report') should be issued in connection with a limited review of interim financial information of a publicly held company.

Choice 'c' is incorrect. Special reports are not issued in connection with the application of accounting principles to specified transactions.

Choice 'd' is incorrect. An auditor may compile, examine, or apply agreed-upon procedures to limited use prospective financial statements (PFS) such as a financial projection, but this would not constitute a special report.

When engaged to express an opinion on a nonissuer's internal control, an accountant should:

Choice 'a' is correct. An auditor should obtain management's written assertion about the effectiveness of the entity's internal control.

Choice 'b' is incorrect. The accountant should disclaim (not qualify) an opinion on management's assertions that the cost of correcting weaknesses exceeds the benefits.

Choice 'c' is incorrect. The accountant has no responsibility to evaluate the effect of subsequent events. In fact, the report on an entity's internal control specifically states that projections of the internal control evaluation to future periods is inappropriate.

Choice 'd' is incorrect. The accountant does provide an opinion (and not a disclaimer) on the effective operation of internal control.