The CAMS-FCI exam validates your expertise in conducting advanced financial crimes investigations within the Acams framework. This credential is designed for compliance professionals, investigators, and financial crime specialists who need to demonstrate mastery of complex investigation methodologies and typologies. This page outlines the exam structure, core topics, and effective preparation strategies to help you succeed on the Advanced CAMS-Financial Crimes Investigations assessment.

Use this topic map to guide your study for Acams CAMS-FCI (Advanced CAMS-Financial Crimes Investigations) within the Advanced Financial Crimes Investigations path.

The CAMS-FCI exam uses multiple question formats to assess both foundational knowledge and applied judgment in real-world scenarios. Questions progress in complexity to reflect the practical reasoning required in advanced investigation roles.

Effective preparation requires a structured approach that maps study time to exam topics and builds confidence through practice. Allocate 6-8 weeks for comprehensive review, balancing conceptual learning with scenario-based problem solving.

Explore other Acams certifications: view all Acams exams.

Strengthen your preparation with up-to-date resources from validexamdumps.com. These materials align to CAMS-FCI and cover practical scenarios with clear explanations.

Visit the exam page to download the PDF, Online Practice Test, or get a Bundle Discount offer for both formats: Advanced CAMS-Financial Crimes Investigations.

Financial Crime Typologies Intermediate and Leading Complex Investigations typically account for the largest portion of the exam, reflecting their criticality in real-world investigation work. However, all four domains are tested, and weakness in any area can impact your score. Balance your study time proportionally while ensuring you have solid foundational knowledge across all topics.

Investigation cases begin with typology recognition (identifying the crime type from red flags), move into complex investigation design and execution, generate findings that must be reported through SARs, and operate within governance frameworks that ensure quality and compliance. Understanding these connections helps you answer scenario questions correctly and apply knowledge practically on the job.

Many candidates confuse similar typologies or miss subtle red flags in scenario questions because they rush through case details. Others struggle with SAR preparation questions by focusing on what to report rather than why and when. Review explanations carefully after practice tests to identify your specific weak patterns and adjust your study focus accordingly.

Read the entire scenario first to understand the full context, then identify all red flags and applicable typologies before selecting your answer. Avoid choosing the first plausible answer; instead, evaluate all options against the specific facts presented. This deliberate approach takes a few extra seconds but significantly improves accuracy on complex cases.

Focus on timed practice tests and review of previously missed questions rather than re-reading study materials. Take at least one full-length practice exam under realistic conditions to assess your pacing and identify any remaining knowledge gaps. In the final 2-3 days, review key definitions, typology characteristics, and SAR requirements to keep concepts fresh without overloading your memory.

The training department is conducting awareness training for unusual customer identification scenarios. Which two indicators should be included? (Select Two.)

This information can be found in the Certified Anti-Money Laundering Specialist (CAMS) study guide, 6th edition, under the section on Unusual Customer Identification Scenarios. The guide explains that two indicators that should be included in awareness training for unusual customer identification scenarios are:

A . The customer opens the account in the name of a family member who begins making large deposits.

This is an indicator of potential structuring, where a customer may be attempting to avoid triggering reporting thresholds by depositing funds in smaller amounts over time. It is important for staff to be aware of this scenario and to monitor accounts for potential suspicious activity.

B . The customer's name and home address cannot be verified.

This is an indicator of potential identity theft or other fraudulent activity. If a customer's identifying information cannot be verified, it is important for staff to conduct additional due diligence to ensure that the customer is legitimate and that the account is not being used for illicit purposes.

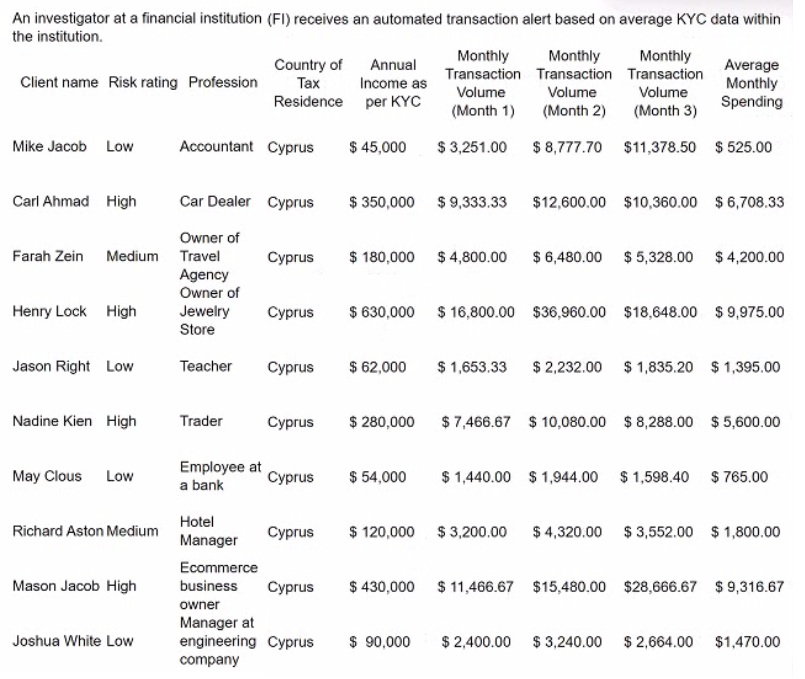

Refer to the exhibit.

In a review of the account activity associated with Nadine Kien, an investigator observes a large number of small- to medium-size deposits from numerous individuals from several different global regions. The money is then transferred to a numbered company. Which is the next best course of action for the investigator?

The next best course of action for the investigator is to file a SAR/STR on the account activity in relation to a potential funnel account. This is because a funnel account is a type of money laundering scheme that involves depositing funds from multiple sources into a single account, and then transferring them to another account, often in a different jurisdiction. A funnel account can be used to conceal the origin, ownership, and destination of illicit funds, and to evade currency transaction reporting requirements. The investigator should report the suspicious activity to the relevant authorities and document the findings and actions taken. The other options are incorrect because:

A . Completing the monthly review and noting the activity for next month's review is not sufficient, as it delays the reporting of a possible money laundering scheme and exposes the financial institution to regulatory and reputational risks.

C . Recommending the account for exit due to frequent global transactions is not appropriate, as it does not address the underlying issue of potential money laundering and may alert the customer of the investigation.

D . No further action is required as the customer is already rated at high-risk and the monthly spending is within expectations is not acceptable, as it ignores the red flags of a funnel account and fails to comply with the anti-money laundering obligations of the financial institution.

Advanced CAMS-FCI Certification | ACAMS, Section 2: Investigating Financial Crimes, page 9

Leading Complex Investigations Certificate | ACAMS, Module 2: Identifying Red Flags, page 5

Which test should be included in a bank's Office of Foreign Assets Control sanctions screening audit program?

The OFAC sanctions screening audit program should include the requirement that all clients with foreign identification are subject to enhanced due diligence, as this provides an extra layer of protection against potential violations of OFAC sanctions.

Which are primary purposes of Financial Action Task Force {FATF)-Style Regional Bodies? (Select Two.)

The primary purposes of Financial Action Task Force (FATF)-Style Regional Bodies are to promote effective implementation of FATF recommendations and to provide expertise and input in FATF policy-making. (CAMS Manual, 6th Edition, Page 180)

A financial institution (Fl) banks a money transmitter business (MTB) located in Miami. The MTB regularly initiates wire transfers with the ultimate beneficiary in Cuba and legally sells travel packages to Cub

a. The wire transfers for money remittances comply with the country's economic sanctions policies. A Fl investigator on the sanctions team reviews each wire transfer to ensure compliance with sanctions and to monitor transfer details.

An airline located in Cuba, unrelated to the business, legally sells airline tickets in Cuba to Cuban citizens wanting to travel outside of Cuba. The airline tickets are purchased using Cuban currency (CUC).

The MTB wants 100,000 USD worth of CUC. Purchasing CUC from a Cuban bank includes a 4% fee. The MTB contacts the airline to ask if the airline will trade its CUC for USD at a lower exchange fee than the Cuban bank. The airline agrees to a 1% fee. The MTB initiates a wire transfer to the airline which appears as normal activity in the monitoring system because of the business' travel package sales.

The investigator recommends that a SAR/STR be filed. What documentation should be referenced in the SAR/STR filing? (Select Three.)

The most likely reason for conducting a reverse transaction is to conceal or launder illicit funds. A reverse transaction is a transaction that reverses a previous transaction, such as a refund, a chargeback, or a cancellation. Reverse transactions can be used by money launderers to obscure the source, ownership, or destination of funds, or to create false records or invoices. For example, a money launderer may initiate a wire transfer from a high-risk jurisdiction to a low-risk jurisdiction, and then reverse the transaction after receiving confirmation of the funds. This way, the money launderer can create a paper trail that shows legitimate funds coming from a low-risk jurisdiction, while hiding the true origin of the funds.